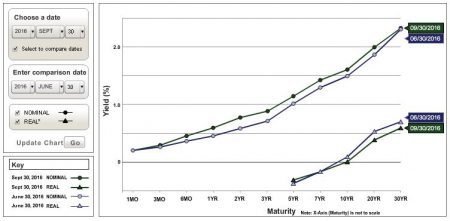

U.S. Treasury Yield Curve Nominal and Real Q3 2016 vs. Q2 2016

At the end of the 3rd quarter of 2016, U.S. Treasury yields, on a nominal basis, were essentially unchanged at the shortest and longest ends, moving up a tad, as much as 20 basis points or so, for all maturities between. On a real basis, for maturities of 5 years or more, yields at the shortest end were more or less unchanged, with rates for maturities 20 years and more up a few basis points.

Interest may affect commercial property economics in numerous ways (see this, this, and this). Borrowing costs are affected directly, with higher interest rates increasing the cost of borrowing and therefore (can) negatively affecting demand. Cap rates generally move with interest rates, although not in lockstep, with considered analyses generally seeming to conclude that capitalization rates on average move in the direction of 10-year rates, but only about a third as much. Interest rates affect the economy, which in turn affects vacancy and rents. In short, the interest rate environment is highly important to commercial real estate investment.

View more yield curve quarterly snapshots.